Management accounting is a very broad concept. Wikipedia characterizes it as an ordered system for identifying, measuring, collecting, registering, interpreting, summarizing, preparing and providing information and indicators important for decision-making on the organization’s activities for the organization’s management link.

The main objective of management accounting is to show the plan and the fact on the financial model of the organization for making management decisions. But how to take into account all the factors and risks for building financial models?

What awaits you in the article

As we approach the formation of management accounting, we forecast costs and determine the minimum planning horizon.

Who is the article for?

The article will be of interest to top managers, project managers, financial managers and everyone who is somehow engaged in calculating the profitability of software production.

Disclaimer

This article is not a panacea, but only a description of the management accounting model that we use to forecast production finances ( Evgeny Lobanov , CEO of AGIMA ).

Management accounting model

Previously, we did not think about what management accounting is used for and how to predict it. There were several related tablets in Excel, where all cash flows were taken into account, but this did not help in making management decisions. The plan fact often diverged, moreover. We decided to formalize management accounting and the procedure for working with it.

There are two main approaches to management accounting:

- Cash flow.

- On closed accounting acts.

It is correct to use the second approach and take into account only closed acts, both in revenue and in costs. Cash flow accounting does not reflect the real financial model of the company. You may encounter an unforeseen situation. For example, you did not fulfill the terms of the contract and the client took the prepayment (and you have already distributed it). In AGIMA cashflow has been moved to a separate system, which is much simpler than management accounting, but we will describe this in the next article.

According to the terms of the agreement with large customers, a deferral of payment is valid from 60 to 90 business days, that is, you will receive payment for your services after 2-3 months. We consider the work completed after receipt of all acts. Closed act = closed work. The costs are similar: for example, in September they paid for furniture (the depreciation period is regulated by the Law), but we will receive the certificate only next month. This means that it will be a cost for October, although the money has already been debited from our account (you can write a motivated refusal to act next month and take the full cost of the furniture).

What is important to consider when forming management accounting

- All costs incurred, including all direct and indirect costs for internal specialists and outsourcing.

- All forecasts for possible future costs, including forecasts for an increase in employee payroll, scaling of the office, taxes, etc.

- We focus only on incoming volumes of work confirmed by documents, without potential orders.

- We keep separate records of all transits, the purchase amount and the mirror sale amount should not be involved in calculating employee motivation.

For example, we performed work for a conditional 100 rubles, while our costs amounted to 50 rubles. Profitability of the task - 50%. If you add 100 transit rubles to them, for example, for a 1C-Bitrix license with a purchase cost of 1C-Bitrix 100 rubles, the profitability will be 25%. This is a deliberate decline in profitability, although nothing really happened.

Cash flow should not affect management accounting. Management accounting must completely coincide, to the penny, with accounting reports ( P&L ), otherwise you cannot trust either one or the other.

The procedure for working with the management accounting model

The procedure for working with the management accounting model consists of five main actions:

- Forecasting the volume of incoming work.

- Validation and cost planning.

- Calculation of quotas.

- Defining a planning horizon.

- Fixing the result of past periods.

1. Forecasting the volume of incoming work

We validate accounting incoming work and determine the probability of occurrence and the degree of influence of risks on the stages of these works. We minimize risks where possible, and fix a clear path to minimize. Or we take out these works for the period of time for which we are building a model.

We forecast direct costs for this volume of work based on the profitability coefficient, which is laid down in the rates for each project participating in the volume of work. In our company, the specialists of the project office and the financial division are responsible for this.

We forecast all quotas for indirect costs based on a retrospective: we take data for the last year and increase it depending on the planned sales volume. If this year the sales volume is x1.5 from the past, then the default cost for the next period is multiplied by 1.5 (applies to all indirect and non-production costs: HR, PR, etc.).

What else to consider:

It is necessary to make the maximum detail of the entire project in stages, which are closed by acts. Ideally, each stage closed by an act should not last more than a month. Otherwise, the team that has been working on one stage for three months will be profitable only in the last month, and the previous two will be “in the red."

Many large customers are not ready to close financial acts every month, so it is worth considering “interim”: “signing TK,” “signing a concept,” “signing a set of prototypes,” etc. Formally, they have much less evidence that the work is completed and accepted , unlike the accounting act, but on them you can immediately understand customer satisfaction with the finished artifact. And you can measure the profitability of the team every month.

It is important to fix the profitability not only for the project as a whole, but also for each stage of work at each production unit, from the company’s department to the final specialist. We measure the profitability of the company and each department. Inside the departments, we look at the profitability of the departments, in the department - each team leader / art director and specialist in their team. We calculate the norms for the development of a specialist based on his payroll tax (including personal income tax and social tax) + fixed indirect per head + planned profitability ratio.

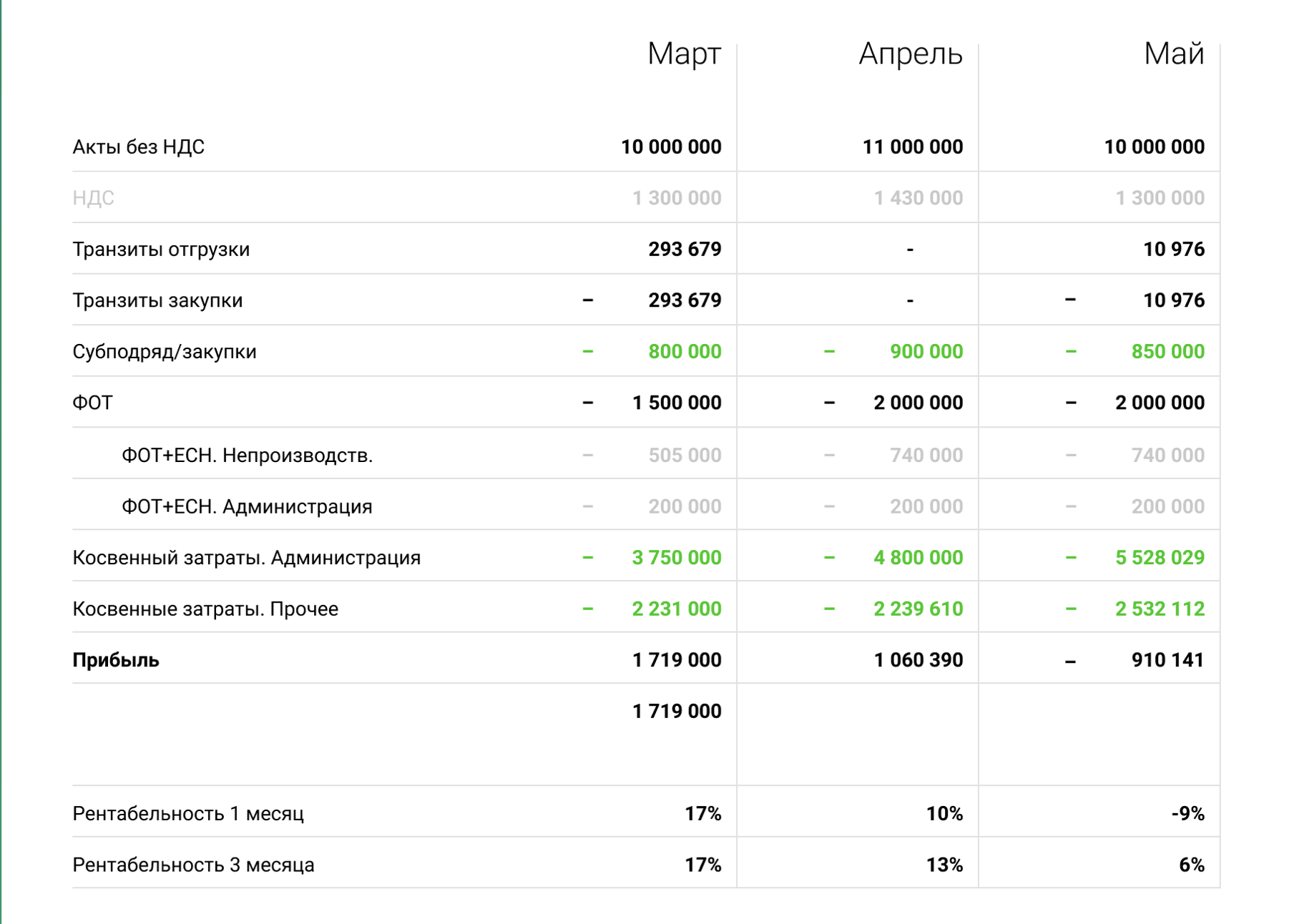

Important: we do not take into account VAT in either volume or cost. This can be seen in the example of a report from our management accounting system.

Uploading a report from our management accounting system. Amounts changed. We generate such reports for each unit.

2. Validation system for plans and forecasts

We distinguish three statuses of work stages:

- Plan (there are all documents, an agreement and orders are signed).

- Forecast (there is an estimate / confirmation from the client of the work, but there are no documents. The agreement is being negotiated with legal entities of the customer).

- Potential (no confirmation and no documents, average statistical deviations for statistical indicators are taken into account).

In management accounting, we take into account only the plan and forecast for the stages of work, without potential (it is used in procedures related to sales).

We determine all stages of work and validate the terms for them:

- We carry out weekly slices for each project from the project office and production: internal deadline of the stage, including validation of the deadlines for each task of the stage, taking into account the time for client acceptance and conducting business testing of tasks.

- We determine the probability of occurrence and the degree of influence of risks at each stage of work.

- We distinguish three degrees of risk: the absence of risk, the risk is probable, the risk is probable and has the maximum impact on the stage (we described the risk map in detail in the article about the ideal time plan).

- We work on risk management of stages with a certain priority.

The main priority of risk management is the volume of the task, the side ones are “long money” (constant work and loading for a long time) and work that we can use as an interesting case. If the volume is small and the task is potentially uninteresting to us, the work can be neglected in management accounting in the risk management procedure.

3. How to plan costs?

This is one of the most important things in management accounting, no less important than working with volumes and revenue. The cost may be something necessary, and something that does not help the company (for example, we are now installing a street infrared heater for smokers. Such a cost will not affect the work of the company, but it will warm our smoking colleagues).

We calculate and fix quotas for regular purchases, determine all cost items:

- We take into account all possible forecasts at once: scalability of the hardware and administrative parts, increase of payroll based on the results of work, indirect forecasts based on legislation.

- Non-production units of the company are also calculated based on the volume of incoming work.

- We introduce quotas in each expense item.

We constantly consider production overhead ( overhead ) and make sure that their ratio does not exceed 1.7. The ideal overhead that we try to adhere to is 1.5.

4. Calculation of quotas in expense items

We plan all costs for the year ahead, calculate and fix quotas for regular purchases, determine all cost items. We repeat, we forecast costs based on a retrospective view, increase quotas depending on the planned sales volume.

To determine the free budget for the planned rate of return, we use the formula:

(Acts + transit volume) - (Indirect + payroll + procurement + transit costs + rate of return).

The profitability indicator for all companies in our market is floating: someone works at 5%, someone under 20%. We allocate this budget to expense items based on the projected profit of each item.

5. How to determine the minimum planning horizon?

First of all, determine the average sales cycle for the last year. It is necessary to transfer potentials to the plan and forecast at least a month before the start of work in order to have time to scale if necessary.

The larger the planning horizon, the better. But the shorter the sales cycle, the smaller the horizon and potential risks. At AGIMA, the minimum required planning horizon is three months, because our average sales cycle is from three to six months (we work in the high price segment, and our customers have a long decision-making cycle). It is also important to validate the availability of work documents, record the period of their preparation and constantly measure the conversion of work statuses from potentials into plans and forecasts. This data is needed to build a model on the minimum planning horizon.

The larger the temporary play, the greater the minimum planning horizon should be. You can’t build a model for one month if the sales cycle is six, - management accounting will be deliberately incorrect.

What does this give us?

When making management decisions, we are guided by numbers. Accounting allows you to build hypotheses. For example, you can see how the indicators change if we take four office managers: we enter data into the payroll (we forecast indirect costs) and see how this will affect the company's economic indicators.

If we see that in three months a large amount of work is expected, and there are not enough people, we begin to look for specialists. The employee selection cycle is from a month to three, and with the manager we can start correcting the situation in a timely manner without waiting for the collapse. By increasing the planning horizon, we identify more predictable risks, put them into management accounting and work with them.

Our profit from effective management accounting:

- We test hypotheses and quickly make decisions.

- We get an additional guarantee that the solution is correct.

- We are building profitability models for each production unit.

- Quickly identify bottlenecks and production crises.

- We constantly strive to increase the planning horizon and identify all projected risks as early as possible.

We believe that management accounting is the most important tool for the operational tracking and impact on the financial condition of any project or company. Build competent management accounting, increase the planning horizon and read our other articles.