The purpose of this article is to show by examples that the events that were discussed at the meeting for the growth of gold liquidity on the exchange market of the Russian Federation will not have the desired effect on the growth in gold trading, if you do not take into account information about the modern nature of trading liquidity, which will actually be discussed speech further in the text.

If you are interested in the topic: why, for example, liquidity for oil on the exchanges of the Russian Federation is far behind the liquidity of oil on the CME and ICE exchanges, then you should continue reading.

Briefly about the meeting

At the meeting, everything went quite mundane: an introductory word from the FAS, a presentation of the Moscow Exchange on events, what is planned to be done and questions and answers on the topic, information that work will continue in the Exchange Committee subcommittee and on which all participants actually dispersed, everything seems to be fine but I still have a feeling that the meeting participants do not have an understanding of the modern nature of the liquidity of the Western market.

My only question was: why is liquidity when trading oil futures on the Moscow Exchange, i.e. volumes and the opportunity to complete a transaction is on the horizon for 2-3 months, but on the exchanges CME and ICE it exists on the horizon of 2 years?

The answer to this question is that there are simply fewer participants on the Russian oil market and therefore the market is not as liquid as on the CME and ICE exchanges and there is a myth about modern liquidity: “The more participants there are on the market, the greater the liquidity is on the market”.

Actually, this myth will be discussed further.

Everything is logical and in reality this factor certainly exists, but the question was: here and now, to sell oil on the horizon of 2 years in the Russian market, i.e. from the answer it follows that due to the greater number of bidders in the West, there are participants who are willing to take the risk of oil prices on a 2-year horizon and they create this demand and supply for oil on a 2-year horizon? Either they did not understand the question, or there is no understanding of the nature of modern liquidity of the 2-year oil horizon.

Before describing the understanding of the modern nature of liquidity, I will give 3 small facts with which I will operate:

Fact 1: The commodity exchange market can be divided into a spot market (where contracts for the physical supply of exchange commodities, such as gold, oil, sugar, coffee, cocoa, wheat, etc.) are traded and the derivatives market (derivative securities, usually futures, for example, the purchase of 1 oil futures is to buy the right to buy oil at the transaction price for a specific date in the future / on the expiration date).

Fact 2: On the western stock market, there are about 60,000 paper barrels per futures / derivatives on world markets per 1 physical barrel of oil (I found an oil slide on the FAS website where the ratio is less, but in general the fact is that the spot trading market has oil an order of magnitude lower than the FAS slides in the derivative oil market, a reference at the end of the article).

Conclusion : the derivatives market is much larger than the spot goods market, since the derivatives market covers the needs of consumers for 1-2 years in advance, and the spot market has only 2-3 months and it is obvious that, due to the size of the market, it is the derivatives market that plays the main role in pricing for commodities, since this market is orders of magnitude larger.

For this reason, the liquidity of commodities is determined mainly by the derivatives market, and not by the spot market, i.e. participants in the derivatives market play a large role in pricing, as they trade large volumes.

Fact 3: From the experience of trading on the ICE and CME exchanges, as a professional trader, over the course of the year I came across the fact that TOP-1 or TOP-2 in terms of volumes of sugar futures contracts for trading on ICE is an English trading company that operates with the amount of guarantee coverage on the exchange about 100-200 million dollars, i.e. in fact, a medium-sized company is the bidder that takes risks on the cost of sugar in the horizon of 1-1.5 years (sugar has lower liquidity than oil) in large volumes.

Conclusion: A bidder with a working capital of 100-200 million can trade large volumes in the futures market of a multi-billion dollar commodity exchange and be TOP-1 in futures volume.

How is this possible ?

In short, this is possible, because in the market such participants do not trade in futures, but in calendar spreads - this is a financial instrument that consists of 2 futures of different periods and different directions. For example, if we buy 1 lot of calendar spread oil DEC19 - JAN20, then in one transaction we buy 1 lot of futures in DEC19 and sell 1 lot of futures in JAN20.

Such instruments are on the Moscow Exchange, but they are used for classic transactions, the so-called rolling, when a trader wants to switch from one futures to another in one transaction. For example, a trader has a position and bought (+) 10 lots of oil in the futures on DEC19, he believes that oil will grow, but the growth will be in JAN20, for this he puts a sell order at (-) 10 lots on the DEC19 calendar spread - JAN20 and when executing an order, he has 0 lots left in DEC19, so (+) 10 collapses with (-) 10 lots, and (+) 10 lots of purchase futures appear in JAN20. As a result, the trader transferred the position from December to January and at the same time pays less commission, since the transaction went through the 1st instrument on the calendar spread DEC19 - JAN20.

I don’t know who and when in the West came up with the use of calendar spread trading to trade the so-called risk averse strategies, but I understand that it is the trading of such strategies, using calendar spreads for futures, that causes modern liquidity in futures on horizons of 1-2 years in the markets CME and ICE, including the oil market.

Calendar Spread Details

If you trade oil in futures, for example on CME (Light Sweet, ticker CL,), then the first thing you encounter is the amount of money you need to have in your account to transfer a position overnight (the so-called overnight), for you 1 An oil futures lot needs about 5-6 thousand dollars to have on the account for the so-called guarantee collateral (GO) to the exchange, although within a day the broker allows you to trade one lot if you have at least 1000 dollars.

The reason for this situation is the high volatility of oil prices, for example, when oil prices rise from $ 60 by 1% i.e. 60 cents, we get an increase of 60 points and a trader can win / lose $ 600 on this growth (1 point = 10 dollars). For this reason, when the exchange asks for a transfer of $ 5,000, it assumes an oil volatility of about 500 points and the amount will guarantee the execution of the transaction, because on the market one side always earns and the other loses, and the exchange only guarantees the execution of the transaction using the GO mechanism . Inside the day, the broker allows you to reduce GO, as in the event of a shortage of funds, he simply closes your positions so as not to take risks.

What does calendar spread have to do with it?

The fact is that the volatility of calendar spreads is usually 5-10 times less than the volatility of the futures it consists of, given that these futures have different directions, i.e. 1 leg of the spread is the futures for the purchase, another leg of the spread is the futures for the sale, i.e. to transfer 1 lot of the calendar oil spread (and inside it is 2 lots of oil futures) you need 500 - 1000 dollars for GO.

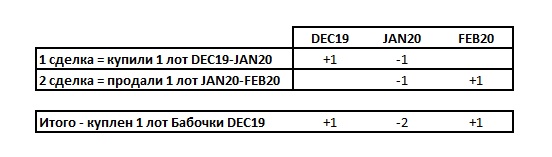

Now let's imagine that you bought 1 lot of the DEC19-JAN20 calendar spread with the 1st transaction and the market went up and you sold the 2nd JAN20-FEB20 spread, so you created a hedge structure that is in the language of traders who trade risk averse strategy, called “butterfly”, see the figure below - in the figure 1 lot of “butterfly” in oil is bought (inside the butterfly, as you know, 4 lots of oil futures).

This design has a price, and if you opened both deals on limit orders, then this is already a profitable deal, since a butterfly is (+) 1-2 points cheaper than you can buy such a design with market orders on the market.

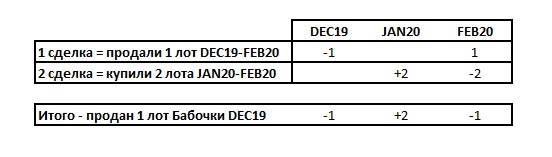

The next step is to disassemble the structure, and they take it apart collecting a butterfly for sale, for example, they sold 1 lot of DEC19-FEB20 before the oil market fell, then after the market bought 2 lots of JAN20-FEB20 (there may be other options for collecting the structure).

As a result, you closed yourself by assembling the structure in the opposite direction and recorded profit from such a transaction in your account.

Why these details? the fact is that the volatility of such hedge structures is even less than spreads and to transfer 1 lot of a butterfly (in which 4 lots of oil futures) you need only 250-300 dollars of GO.

That is, when trading 1 oil futures for transfer overnight, you need to have $ 5,000 GO on your account, if you trade oil futures through calendar spreads, you need $ 50-80 GO for 1 lot of futures in a butterfly, ten times less.

Another important point on spreads

Collecting a butterfly design for a purchase at a price of (+) 10 for example, then you collect a butterfly design for a sale at (+) 11 and then you will earn 4 transactions (+) 1 point or 10 dollars, while making a profit from this exchange you should take a commission less than these 10 dollars of profit from you, and after all 4 lots of futures participated in transactions, in fact, they were bought and sold in different periods and for individuals it will cost about 16-18 dollars for a commission to the exchange.

That is why professional traders exchange commission for such transactions should be 1-1.5 dollars per circle (usually called rebates from the exchange for the volume of transactions) or 4-6 dollars, then for these 4 transactions the trader will earn 10 - 6 = 4 dollars. And so, in order to earn 200 - 400 dollars on 4 transactions, the trader begins to trade not 1 lot in hedge designs, but 20, 50, 100 lots or more and here VOLUME or liquidity appears.

If you bought 100 lots of butterflies, then you have GO = 800 dollars, and 400 lots of oil futures in 3 periods hang on the futures curve: (+) 100 (-) 200 (+) 100.

There are other examples of hedge designs: condor (an example of buying 1 lot of condor is obtained on the futures curve (+) 1 (-) 1 (-) 1 (+) 1, i.e. it covers 4 periods and contains 4 futures), combo (example 1 lot combo is on the futures curve (+) 1 (-) 3 (+) 3 (-) 1, it also covers 4 periods and contains 8 futures).

Total on calendar spreads: I think this example gave an understanding of how a trading company with a working capital of $ 100 million became the TOP-1 in sugar trading on ICE futures. In fact, the reason for this is the risk averse strategy trading by traders - “wholesalers” who, due to the fact that they trade in slightly volatile hedge structures (conditionally, “piping” slangs) and to earn money, trade in large volumes using calendar spreads, fixing their deals as “cement” the entire futures curve at different time periods.

Such a “cementing” of the futures curve by a large number of bought and sold futures in a large number of periods reduces the volatility of a commodity on large horizons due to speculative activity and if it is generated, it is due to the presence of objective factors in the macroeconomics of the commodity industry.

On the other hand, such a “cementing” of the market makes it possible for such “wholesalers” traders to make money anyway, because they still buy or sell, it’s clear that in order to assemble a design at a reasonable price, it is important to stand in the direction of the market within the next 2-3 hours For example, if the front futures of oil goes up by 10-20 points, then the first leg of the structure should start with the purchase, as soon as the market grows the front futures by these 10-20 points, then in the spread it will move up by 1-2 points, then it stands on the limit order for pro azhu open 2nd leg design.

Such micro-oscillations in the spread are enough to assemble the structure at a bargain price, the next step is to assemble the same structure in the other direction only.

That is why traders, "wholesalers" do not care where to sell and buy, at

the fact that in this one period they buy, and in the other they sell using calendar tools as derivatives of derivatives. And for the most part, it is their orders that are in the “glasses”, and not market makers who are willing to stand up for the money in the “glass”.

This is the modern nature of liquidity in futures and this can be considered as one of the reasons why the market often does not go up or down, but more so as a sideways movement. Because traders who trade such strategies in order to enter limit orders need the market to go up, for example, and then down or vice versa, and they certainly contribute to such market movement within the day when trading large positions.

If the market went against the trader, then the trader receives a hedge structure at a low price at the stop order, i.e. remains in the market and he has a chance to disassemble this unprofitable structure and go to zero and not fix the loss.

It may seem that it’s easy enough to make a profit, but the practice is usually for 10 designs 3-4 profitable, the rest have to be disassembled by the cost of entering the market. So the trade of such structures is also a risk, but acceptable and controlled, because with such a trade no one takes the risk of trading long horizons

The history of trade shows that the prices of futures of neighboring months rarely scatter in different directions. There are exceptions, of course, on seasonal commodities, for example, natural gas spreads March-April, October-November - I would not recommend using these winter-summer transitions even in hedge designs. Or another example in agricultural crops (cocoa, coffee, wheat) there the spreads between different calendar years can also greatly depend on the vagaries of the weather.

In general, this approach to trading works and traders “wholesalers” often serve as the other side of the transaction for consumers and producers of commodities, just everyone earns their “bread” in different ways. It’s not worth considering that such strategies make it easy to make money: out of 10-15 traders who start trading such strategies, 1-2 people remain in professional trade in a couple of years, while the rest cannot make money from such trading.

Instead of a conclusion

If we want to increase liquidity in Russia, for example, in the oil market, then it is worth considering:

- Increase the number of calendar spreads on the exchange. There are calendar spreads on the Moscow Exchange, but in order to trade such strategies in oil at least on the horizon of 1 calendar year, they should have 12 * 12 = 244 calendar spreads, and not 3-4 calendar spreads for rolling;

- Change IT platform. The Moscow Exchange needs to change the IT platform and infrastructure, where simultaneously deals on calendar spreads (400 - 500 instruments) and 10-20 futures in oil and 400-500 instruments in the form of oil options in a cycle / round of information for 20-30 milliseconds should be combined . Maybe this is the Moscow Exchange? I don’t know, but I think developers in Russia have someone who can create / repeat the experience of CME and ICE with such a trading platform;

- Rebate. The Moscow Exchange should have appropriate discount policies on commissions or rebates for professional traders so that it is profitable to trade such strategies;

- Terminals We need specialized specialized terminals, since spreads trade not from the chart, but through matrices;

- Support for complex orders. These other trading terminals must support complex orders that allow you to enter the market under different conditions and for several instruments;

- Increase bidding time. We need a different trading mode, not from 10.00 Moscow time to 23.49, but 1 hour break per day, as on CME, for example;

- Preferences of traders from other time zones. Preferences are needed for trading companies who trade in another time zone, when the Russian Federation is sleeping, the market can be traded by those who are in Latin America or China, for example, this is necessary to maintain liquidity on a 24-hour basis;

- Preferences for long periods of trading. The further the deals are made along the curve, the greater the volume discounts for these distant periods;

- "Pro-rata" mixing method, not FIFO. Combining transactions in calendar spreads should be proportional to the size of placed orders: for example, there are 1000 lots for sale and someone buys 100 lots from this 1000 lots, then transactions should not be reduced with those who placed the order in the “glass” of transactions, but in proportion to the volumes positions - this motivates placing large volumes of orders for traders and it is difficult to turn the level in such a situation, i.e. moving the market becomes harder.

Here are 9 points that came to mind that you should pay attention to liquidity in the oil market in Russia by analogy with CME and ICE. Most of these points are tied to IT implementation, which is why I chose the Habr site to publish this article, because the IT specialist in the 1st specialty himself believes that there are such people and resources in the Russian Federation who can do this, but everything always rests in organizing this process.

It should be understood that the problem of liquidity in the oil market in the Russian Federation is not that supply futures, as was discussed at the meeting, namely, the underdevelopment of the derivatives market of the Russian Federation and the absence of such tools as calendar spreads. For example, with deliverable futures, “wholesalers” traders who trade such strategies simply close their positions in 1-2 days according to the risk management policy in their companies and therefore deliverable futures or non-deliverable ones are not important.

And back to the gold

Gold is not traded in calendar spreads. And most likely the reason is that gold has always been considered a competitor to the dollar, and it is precisely in the dollar, namely, in the interest rates for the dollar on the EURODOLLAR instrument (on CME, not to be confused with the EUR / USD currency pair) that has the highest liquidity by horizon: about 5-7 years, quarterly spreads are traded there.

Only one fact is that in the “glass” of EURODOLLAR for the first 3 years in the quarterly spread there are an average of 50,000 - 100,000 lots, where 1 lot of EURODOLLAR futures is a contract to lend or borrow 1 million dollars at quoted interest rate, then already on this fact you can understand the reason for the strength of the dollar as a world currency. And such liquidity is available around the clock.

We all think we heard the story of how, during the time of Roosevelt, during the depression they seized physical gold from the Americans, in fact they removed the alternative to the dollar from circulation.

And now, when the dollar begins to lose ground, and there is a tendency towards regionalization of the world economy, discussing which regional currency zones may appear, then gold starts to be considered again as an alternative monetary unit.

Given the physical limitation of the amount of gold, many believe that it has little chance, on the other hand, developing the gold trading with derivative instruments, the issue of gold shortage is being addressed, since you can drive any amount of money into the gold futures curve under the price of gold and there are examples of the futures curve EURODOLLAR, oil (not in vain for 1 physical barrel of oil 60,000 barrels of paper).

A number of points were discussed at the meeting:

1. To provide a link / interconnection of the Moscow exchange platform with London and Beijing. Yes, it will help in liquidity in the spot market, it will not help in liquidity in long periods

2. Oblige to sell gold to gold miners. It is possible so, but what about market pricing mechanisms? Maybe it’s better to develop derivatives on gold? For example, there are many small gold miners in alluvial gold who can fix the price of gold for the next mining season using the liquid futures curve, for this certainty, finance the purchase of fuel, materials, spare parts and import it through the winter road and extract this gold and bring it to market.

For information: TOP-25 gold mining companies in 2018 are closed by a company with a production volume of 1,300 kg, which means we have hundreds of such small companies who, with such certainty in gold prices, can be financed for this certainty, since the mining economy is placer gold is simple enough

3. To help large gold miners to remove the restriction from banks to sell gold mined only to banks that have funded this business. What for? To trade derivatives, you only need money and it doesn’t matter whether gold is pledged or not, and liquidity over large horizons allows you to hedge price risks even if gold is pledged, the main thing is that the money be under GO.

PS: I caught myself thinking when I listened to the performance of the representative of the Moscow Exchange at the FAS, and the Moscow Exchange is essentially our monopolist on the Russian exchange market, that the place for the performance is right - the building of the FAS (Federal Antimonopoly Service) ...

But something will move on, wait and see

Link to FAS presentation, slide 8 on oil