US regulators prohibit the distribution of the Telegram Open Network token

Tonight, a press release from the Securities and Exchange Commission (SEC) appeared that they filed a complaint against Telegram Group Inc and TON Issuer Inc for violating the terms of the preliminary placement of claims for tokens.

What does this mean, how serious is it, and what will happen to the whole project now, we will try to figure it out together, based on the available facts.

This is not the first, and most likely not the last case, when the SEC claims against distributors of crypto tokens. Since the summer of this year there have already been three high-profile processes:

In all three cases, the claims are the same: you conducted a public sale of “securities” (security in the original) on the American market, and this imposes additional requirements on the legal entities involved in this, namely reporting, informing investors, disclosing financial indicators and all that there is a whole list.

At the same time, it can be objected that the tokens being sold are simply “candy wrappers” intended for internal calculations and bear no value. To separate the “candy wrappers”, which can be sold as ordinary goods, without additional regulation, and the “shares”, which are securities and therefore fall within the SEC's area of interest, the so-called Howey Test is used. These are four signs that a security has: it must be purchased for money (cryptocurrencies, according to the 2017 amendment, are also considered money); the purpose of the acquisition is the expectation of profit; the seller of the paper is an existing organization and profit will be received without the participation of the investor (due to the actions of the seller or third parties).

The following clause was in the token sale agreement:

It was assumed that such a refusal of any financial responsibility to investors means that utility tokens are sold. In this case, the SEC could simply ignore the sale as being outside its competence or even formally make a statement that it does not consider GRM tokens as securities, which would be generally wonderful.

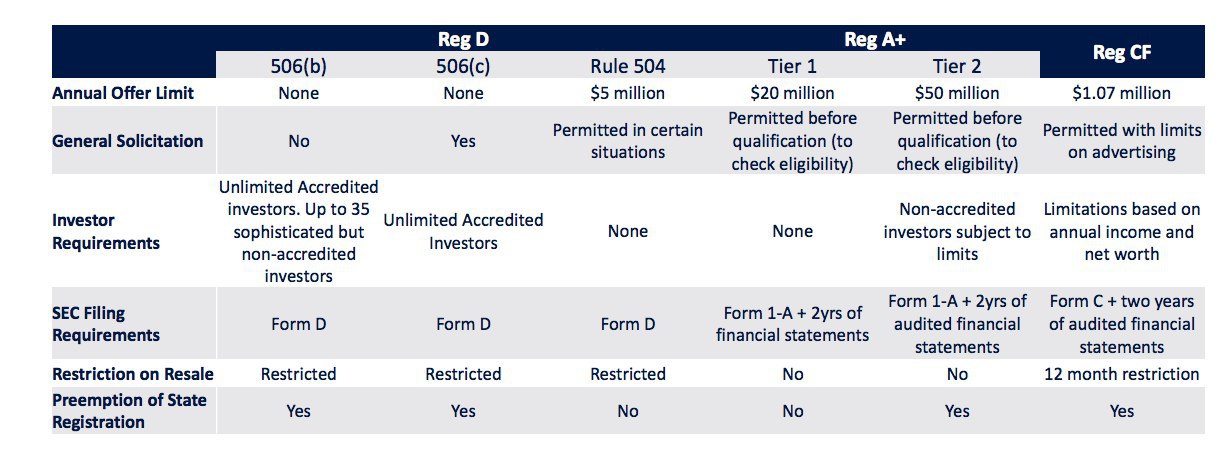

There is a list of exceptions when you can even sell securities without SEC control:

In the case of TON, it was an excuse 506 (c), imposing restrictions on the resale of the received "values" and requiring work only with qualified investors (verified by identity, with proven experience in the financial market, and so on, there are their own requirements). The sale of the “right of demand” (agreements with investors) on tokens not yet issued is, of course, a sale of securities and therefore the necessary actions have been taken, namely, a notice of sale has been submitted under exception 506 (c).

By the way, in this very notification the purpose of fundraising was indicated and this is “the development of the TON blockchain, payment of current expenses and the development of the Telegram messenger, as well as other expenses”. And there are not so many expenses there, but decent, 100-200 million could easily come running in a couple of years. It may be that money for a full refund to investors is no longer enough, since over two years of other expenses it could accumulate fairly. However, I personally think that Pavel should have a couple of hundred million to cover current expenses, and no one touched the money of investors.

Investors are designed as expected, tokens do not give us the right to company profits, which means they are suitable only for internal use, which means that utility will definitely be recognized. But now this morning it has become much worse. The fact is that in a complaint sent to a court in New York, the text of the SEC regarding GRM tokens (in conclusion, at the end of the file) is stated in plain text:

This is the official position of an official body expressed in an official document. What does this mean for Telegram?

In March, the following consideration was voiced for investors:

However ... maybe it’s true that it happened in similar situations?

The SEC has been demanding sanctions against Kik Interactive for a very long time, including based on the fact that in many other cases such processes ended with the sentencing. KiK's position is denial, they say our tokens are not secured, but we ourselves are white and fluffy. True, the position is weak, they talked a lot and wrote about profits awaiting buyers of miracle tokens. It was not possible to reach a pre-trial decision, the proceedings are ongoing, but the company has already had to turn off its messenger . Something tells me that such a scenario is not very suitable for Durov.

The story with Block.one, an EOS developer, ended better. They managed to reach a pre-trial settlement of the dispute by paying a fine of 24 million for their multi-billion dollar ICO. They insisted that they did not know that they were breaking the law, emphasized that the tokens in question (ERC-20) were frozen after the launch of the main network, that is, they went out of circulation, and that the sale was organized for ether tokens (cryptocurrency) before how such sales began to fall under the jurisdiction of the SEC. At the same time, they did not admit their guilt, they simply asked to withdraw all claims. The story ended well for Block.One, but I draw your attention - the case did not go to court, and Telegram has already filed an application for consideration of the case ... So, probably, you should not count on such an outcome.

Such facts, now let's think about who is to blame, what to do and what awaits us in the near future.

Firstly, we must wait for the decision of the court and the actions of Durov. You can speculate and speculate as much as you like, everything can be very different, you have to wait for the situation to develop. There is little doubt that the court will accept the arguments of the securities commission, but still the utility of the essence of GRM tokens is expressed quite strongly. Again, it depends on the actions of the Durov team, maybe they can convince the SEC to limit themselves to a fine for an improper sale (although everything seems to be in order, claims to the platform) and then the situation will develop according to the EOS pattern. But it seems unlikely to me.

Further, after the requirements in the SEC take effect, Pavel Durov has two equally unpleasant choices:

Well, all possible options between these two extremes, for example, in words, make regulation in the messenger, through an additional add-on over the network, but at the same time allow alternative clients to remain anonymous (using another workchain, for example). Or refuse to make changes to the blockchain, but remove it from the telegram, developing as a separate legal entity. Wherever you throw - everywhere a wedge.

An important point is that the pre-sale agreement stipulates its automatic termination, with a refund, in case of non-launch of TON until October 31, 2019, that is, within two and a half weeks. Finding 1.7 billion for payment may not be easy even for Durov, but it can be a good solution to take a break, modify the technology and interfaces a bit (now everything is extremely raw) and think about what to do next (the simplest is to conduct Initial Exchange Offering on which -any exchange, without the participation of US citizens). I’m not sure that this will allow integrating tokens into the messenger, but at least the project will be able to begin independent development.

In numerous superficial comments, the opinion is expressed that "there is nothing to worry about, we will drive these pendos and live." This is not true. The problem is not that you need to return money to American investors and abandon the possibility of working in the US legal field. The problem is that after making such a decision, the TON network becomes officially “outlawed”. The law of the United States of America, but, in fact, in a controversial situation, this will be the strongest argument not to deal with similar entities. The network cannot be integrated into the Telegram messenger, it cannot be swiped out on exchanges, it will not be possible to integrate into official payment channels. It is necessary to act very carefully and carefully now, I hope that Pavel Durov foresaw this situation and prepared, at least approximately, in which direction to move.

We will follow with interest.

Update: Investors received a letter (I didn’t find a more decent link with a letter in the public domain, but the letter is real) that the company was surprised that the case immediately went to court, as it was constantly in touch with the SEC and was ready to listen and take into account their claims . It’s good that Telegram “disagrees”, apparently that the launch and distribution of grams is a settled issue, it remains to find out how white (corresponding to the requirements of regulators) the circuit will be.

What does this mean, how serious is it, and what will happen to the whole project now, we will try to figure it out together, based on the available facts.

This is not the first, and most likely not the last case, when the SEC claims against distributors of crypto tokens. Since the summer of this year there have already been three high-profile processes:

- At first, in the beginning of June, it was the case of KIK Interactive , the messenger developers who raised about one hundred million dollars in 2017 for their tokens.

- Then, at the end of September, claims to Block.one, the creators of the EOS platform, who, it seems, collected six billion during the year, ended with a pre-trial settlement .

- And today there have been complaints against the Telegram , the case has been sent to court.

In all three cases, the claims are the same: you conducted a public sale of “securities” (security in the original) on the American market, and this imposes additional requirements on the legal entities involved in this, namely reporting, informing investors, disclosing financial indicators and all that there is a whole list.

At the same time, it can be objected that the tokens being sold are simply “candy wrappers” intended for internal calculations and bear no value. To separate the “candy wrappers”, which can be sold as ordinary goods, without additional regulation, and the “shares”, which are securities and therefore fall within the SEC's area of interest, the so-called Howey Test is used. These are four signs that a security has: it must be purchased for money (cryptocurrencies, according to the 2017 amendment, are also considered money); the purpose of the acquisition is the expectation of profit; the seller of the paper is an existing organization and profit will be received without the participation of the investor (due to the actions of the seller or third parties).

The following clause was in the token sale agreement:

the Purchaser is not entitled, as a Party to this Purchase Agreement, to vote or receive dividends or be deemed the holder of shares of the Issuer or the Parent for any purpose, nor will anything contained> be construed to confer on the Purchaser, as such, any of the rights of a shareholder of the Issuer or the Parent or any right to vote for the election of directors or upon any matter submitted to shareholders at any meeting thereof, or to give or withhold consent to any corporate action or to receive notice of meetings, or to receive subscription rights to purchase shares of the Issuer or the Parent or otherwise "Buyers will not receive any dividends, shares in profits and other benefits related to control over the company

It was assumed that such a refusal of any financial responsibility to investors means that utility tokens are sold. In this case, the SEC could simply ignore the sale as being outside its competence or even formally make a statement that it does not consider GRM tokens as securities, which would be generally wonderful.

There is a list of exceptions when you can even sell securities without SEC control:

In the case of TON, it was an excuse 506 (c), imposing restrictions on the resale of the received "values" and requiring work only with qualified investors (verified by identity, with proven experience in the financial market, and so on, there are their own requirements). The sale of the “right of demand” (agreements with investors) on tokens not yet issued is, of course, a sale of securities and therefore the necessary actions have been taken, namely, a notice of sale has been submitted under exception 506 (c).

By the way, in this very notification the purpose of fundraising was indicated and this is “the development of the TON blockchain, payment of current expenses and the development of the Telegram messenger, as well as other expenses”. And there are not so many expenses there, but decent, 100-200 million could easily come running in a couple of years. It may be that money for a full refund to investors is no longer enough, since over two years of other expenses it could accumulate fairly. However, I personally think that Pavel should have a couple of hundred million to cover current expenses, and no one touched the money of investors.

Investors are designed as expected, tokens do not give us the right to company profits, which means they are suitable only for internal use, which means that utility will definitely be recognized. But now this morning it has become much worse. The fact is that in a complaint sent to a court in New York, the text of the SEC regarding GRM tokens (in conclusion, at the end of the file) is stated in plain text:

Due to Messenger's infrastructure and other features that permit anonymous communications and transactions, once Grams are distributed to the public, it may be difficult, if not impossible, to trace who has purchased Grams and / or to know who is a current investor in Grams. Although Telegram contemplates requiring Messenger users to fulfill certain “Know Your Customer / Anti-Money Laundering” requirements for users to use future services, Telegram has stated that it “will have no access to this information.” Moreover, it is uncertain whether identification of parties to transactions in the secondary market for Grams will be ascertainablethe technology allows you to remain anonymous, and go figure out which pedoterrorists will use it.

The Initial Purchasers' purchases of Grams, and any subsequent purchases of Grams, were and will be an investment of money, in a common enterprise, with an expectation of profits, derived primarily from the current and future entrepreneurial and managerial efforts of Defendants and their agents to build the TON Blockchain and drive demand for Grams. Consequently, Telegram's offer and sale of Grams to Initial Purchasers, and any upcoming, offers, sales, or distributions of Grams were and will be offers and sales of securities.since everyone buys grams to get Xs, then, whatever one may say, this is a security

This is the official position of an official body expressed in an official document. What does this mean for Telegram?

In March, the following consideration was voiced for investors:

If Grams would be classified as securities, it would complicate partnerships with crypto exchanges and make it impossible to provide storage and trading services for Grams in the application of the messenger. Telegram team and Pavel Durov personally are working with SEC and Skadden to reduce this risk.If suddenly grams become “securities”, then they will have to be removed from the messenger, and it will be much more difficult to place them on crypto exchanges. Let's hope that everything will work out.

However ... maybe it’s true that it happened in similar situations?

The SEC has been demanding sanctions against Kik Interactive for a very long time, including based on the fact that in many other cases such processes ended with the sentencing. KiK's position is denial, they say our tokens are not secured, but we ourselves are white and fluffy. True, the position is weak, they talked a lot and wrote about profits awaiting buyers of miracle tokens. It was not possible to reach a pre-trial decision, the proceedings are ongoing, but the company has already had to turn off its messenger . Something tells me that such a scenario is not very suitable for Durov.

The story with Block.one, an EOS developer, ended better. They managed to reach a pre-trial settlement of the dispute by paying a fine of 24 million for their multi-billion dollar ICO. They insisted that they did not know that they were breaking the law, emphasized that the tokens in question (ERC-20) were frozen after the launch of the main network, that is, they went out of circulation, and that the sale was organized for ether tokens (cryptocurrency) before how such sales began to fall under the jurisdiction of the SEC. At the same time, they did not admit their guilt, they simply asked to withdraw all claims. The story ended well for Block.One, but I draw your attention - the case did not go to court, and Telegram has already filed an application for consideration of the case ... So, probably, you should not count on such an outcome.

Such facts, now let's think about who is to blame, what to do and what awaits us in the near future.

Firstly, we must wait for the decision of the court and the actions of Durov. You can speculate and speculate as much as you like, everything can be very different, you have to wait for the situation to develop. There is little doubt that the court will accept the arguments of the securities commission, but still the utility of the essence of GRM tokens is expressed quite strongly. Again, it depends on the actions of the Durov team, maybe they can convince the SEC to limit themselves to a fine for an improper sale (although everything seems to be in order, claims to the platform) and then the situation will develop according to the EOS pattern. But it seems unlikely to me.

Further, after the requirements in the SEC take effect, Pavel Durov has two equally unpleasant choices:

- You can “bend”, add regulation, which will make it possible to fulfill all the requirements of the commission, but then it will not be the TON that was originally created.

- You can “fight” by refusing to meet these requirements, automatically becoming a violator of American laws with all the ensuing consequences, affecting, inter alia, the main project of Pavel - the Telegram messenger. Removing illegal programlins from appstores is a strong blow, how painful only the owner of the messenger knows.

Well, all possible options between these two extremes, for example, in words, make regulation in the messenger, through an additional add-on over the network, but at the same time allow alternative clients to remain anonymous (using another workchain, for example). Or refuse to make changes to the blockchain, but remove it from the telegram, developing as a separate legal entity. Wherever you throw - everywhere a wedge.

An important point is that the pre-sale agreement stipulates its automatic termination, with a refund, in case of non-launch of TON until October 31, 2019, that is, within two and a half weeks. Finding 1.7 billion for payment may not be easy even for Durov, but it can be a good solution to take a break, modify the technology and interfaces a bit (now everything is extremely raw) and think about what to do next (the simplest is to conduct Initial Exchange Offering on which -any exchange, without the participation of US citizens). I’m not sure that this will allow integrating tokens into the messenger, but at least the project will be able to begin independent development.

In numerous superficial comments, the opinion is expressed that "there is nothing to worry about, we will drive these pendos and live." This is not true. The problem is not that you need to return money to American investors and abandon the possibility of working in the US legal field. The problem is that after making such a decision, the TON network becomes officially “outlawed”. The law of the United States of America, but, in fact, in a controversial situation, this will be the strongest argument not to deal with similar entities. The network cannot be integrated into the Telegram messenger, it cannot be swiped out on exchanges, it will not be possible to integrate into official payment channels. It is necessary to act very carefully and carefully now, I hope that Pavel Durov foresaw this situation and prepared, at least approximately, in which direction to move.

We will follow with interest.

Update: Investors received a letter (I didn’t find a more decent link with a letter in the public domain, but the letter is real) that the company was surprised that the case immediately went to court, as it was constantly in touch with the SEC and was ready to listen and take into account their claims . It’s good that Telegram “disagrees”, apparently that the launch and distribution of grams is a settled issue, it remains to find out how white (corresponding to the requirements of regulators) the circuit will be.

For our investors,

As you probably saw, on October 11, the US Securities and Exchange Commission (SEC) filed a lawsuit against the Telegram Group Inc. in the US federal court. and TON Issuer Inc., in an attempt to prevent the launch of the TON blockchain. In accordance with SEC's stated desire to interact with developers of digital asset technologies, Telegram over the past 18 months has tried to interact with SEC and receive feedback on the TON blockchain. We were surprised and disappointed that the SEC decided to file a lawsuit in these circumstances, and we do not agree with the legal position of the SEC.

Together with our consultants, we continue to evaluate the best ways to resolve the situation in the interests of the parties involved, including, but not limited to, evaluating whether or not to try to delay the launch date. We are working hard to quickly resolve these issues, and hope to provide further updates over the next week.

Respectfully,

All Articles