What is known about Walmart Pay, what is unknown Apple Pay

Over the past three years, many developments have occurred in the field of payments - and, more generally, in the field of trade.

PayPal made friends with card networks and their issuers.

India has demonetized its currency and launched a program to introduce digital payments.

Amazon launched voice commerce with Alexa and a portfolio of applications and devices that now put it at the consumer’s disposal.

Selfie Pay has become a reality .

Walmart bought Jet.com to strengthen its e-commerce business.

The quick payment of piecework gave a strong impetus to the development of the economy of piecework earnings.

Payments bring us closer to the day when we can refuse checks ( #killthecheck ).

Efforts to combat fraudsters from the payment ecosystem have reduced online fraud by about a third.

But something has not been done in the past three years: consumers have not been stimulated to use smartphones as a digital form factor of payment when making payments in physical stores.

In fact, the results of PYMNTS / InfoScout “Implementation and use of mobile payments” for the last nine quarters say about the same as before: consumers do not have sufficient reasons not to forget to use them, although they usually hold the phone in one hand in the store while the other take out their plastic card in order to pay at the checkout.

Let's clarify what we mean by “use”: this is the percentage of people who have a payment method on their phone, who pay in a terminal that supports this method, and, finally, those who actually use it to make a purchase.

The reluctance to exchange a leather wallet for an electronic one does not disappear, despite the proliferation of NFC-enabled terminals for “[insert the right name] Pay”, which requires contactless communication to initiate a payment - a rather sobering reality for the “grandfather” of all Pay - Apple Pay - despite the enthusiastic mention of Apple Pay by Apple CEO Tim Cook in their latest earnings report last week.

According to him, Apple Pay can be "currently the number one contactless payment service on mobile devices, which accounts for 90% of all transactions worldwide." But this is very similar to saying that you are the best of all troechnics in a troechnik class: it still remains a troechnik class.

After nearly three years - after all the hype and huge investments in advertising and promotion - Apple Pay cannot count even 6% of its use in the largest payment market in the world.

According to our results, the average use over nine quarters is about 4.5%. Although a maximum of 5.9% was seen, and in the last quarter the figure reached 5.5%, the trend remains unchanged, despite growth in this quarter.

At this stage of his life cycle and the cycle of maturity, the question arises: Will he ever be able to break through this ceiling?

At the end of June, when the next survey was conducted, 24.5% of respondents said that they first tried Apple Pay, compared with 21.9% in March. And 5.5% said they used it to pay for purchases, which is higher than 4% in June, but lower than the maximum in March 2015

It is difficult to understand whether this is the beginning of a consistently growing trend or another jump, but statistically it looked like another random jump along a rather gloomy trend line. When we asked consumers how often they used Apple Pay to pay for a physical store, they responded that they did it about 18% of the time. Since March, this figure has not changed and continues to decline since October 2015.

However, there is one exception to this story: Walmart Pay .

Since March, we have seen how the frequency of first use of Walmart Pay increased by 31.7% to 19.1% of respondents. The number of those who have an application on a smartphone and uses it for payment increased by 53.5% to 5.08% of respondents.

This jump is not interesting in itself, but because of the speed with which Walmart Pay forces those users who tried it for the first time to use it again. The use of 5.03% is observed after only 1 year on the market and this quarter only falls short of the Apple Pay figure of 5.5%, which is already on the market for the third year.

The frequency of using Walmart Pay is also an interesting story.

Nearly 50% (more precisely, 47.2%) of respondents who shop at Walmart say that they used it at every opportunity - only 6.6% said they never thought of using it.

However, this does not mean that before Walmart is not difficult tasks. Walmart Pay's biggest competitor is cash - it’s them, according to consumers, that they used instead of Walmart Pay, and many of them use it to make purchases so far. Ditto EBT cards that can not yet be registered in a digital wallet for payment. These are two big and important issues for Walmart Pay.

However, it seems that the popularity of Walmart Pay does not lie in the very possibility to pay for purchases using the in-app application, but rather in the set of additional functions that accompany the payment process at the checkout.

But this is not even payment in the traditional sense of the word.

In fact, the QR code of Walmart Pay identifies the user before the start of the payment process, after which the consumer can put the phone back in the bag. The process of using coupons, promo codes, Savings Catcher bonuses and gift cards (if any) begins in the app, offering all the choices for the consumer until payment is complete. Walmart Pay also supports mobile grocery ordering, which will bring you to the car window, online purchases and in-store payment in cash, and now a number of financial services, including savings.

It all went much further than Apple Pay, which is still trying to complete this shopping quest (and, it seems, went the wrong way).

Integration of store loyalty programs in Apple Pay sounds tempting - until you get to the point where you still need to stand in line to get to the cashier and pay for it. At this stage, according to our respondents, the use of the card works great, especially since the use of card payment systems when paying for purchases at most stores today is quite fast.

You can say: wait, but after all, Tim Cook during the last teleconference on the company's financial activities, said that 3/4 of Apple Pay transactions occur outside the US, where, according to him, “the mobile payment infrastructure is developing faster than in the US ".

Despite the fact that all innovative payment innovations come from the US (if I read it out loud, you would hear a large share of sarcasm in my voice), can this country lag behind the ubiquitous contactless payment terminals for several years? According to statistics, 52% of US merchants accept contactless payments, including many successful small businesses, such as coffee shops and bakeries, that work with integrated terminals for sale, such as Clover and Square.

Unfortunately, this may not be the reason Apple Pay cannot win consumers in the US - although it could once be a good excuse for the low popularity of Apple Pay in its homeland - and, frankly, I was criticized when reviewing their early strategy. launch a payment system.

How much does Apple Pay account for, and where do consumers use it?

Maybe in the UK, where contactless payment is not very popular?

Maybe in Australia, where large banks tried to block Apple Pay, because they do not want to get into 15 bp. Apple Pay with their own contactless mobile wallets?

Maybe in Japan, where over the past 15 years, no mobile wallet has managed to gain popularity, and where the use of Apple Pay, as in the UK, seems to be a little popular?

Maybe in one of the new markets, such as Sweden or Denmark, where digital payments are an integral part of life, but where are local systems like Swish and Dankort, which are widely used and used today, so popular?

The short answer to this question is that we don’t know and may never know.

The likely answer to this question is unlikely, because if this were actually the case, Apple would have told about it.

Example: Even when Apple listed all the reasons for service revenue in its earnings report last week in response to an analyst's question, everything on this list except for Apple Pay. Nobody returned to this question anymore.

It is well known that Apple Pay is not used in China, where the company is betting on the future and where Apple Pay as a mobile payment solution puts users in touch with promotions and gifts to get them to try the system.

It is clear that China is a priority for Apple as the second largest economy in the world. There is only one problem: Apple has not become a top priority for China.

As a company, Apple has been losing sales in China since 2012, which fell by 10% in the last quarter, after a decrease of 14% from the previous quarter. Apple has a share of ~ 9% in the mobile phone market in China and a 0% share in the payments market (I think the numbers have just been rounded down!), According to a study conducted by China Channel . In China, Apple is considered a luxury brand, but now it’s one of the many phones that Chinese consumers buy to access the most important things for Chinese consumers: WeChat and the rest of the chat rooms, games, and commercial applications of the mobile ecosystem.

According to the China Channel report, 67% of Chinese consumers use QR codes from Alipay or WeChat Pay to pay at the store, 22% use UnionPay cards and 11% use cash (and zero percent use Apple Pay). When 4,000 Chinese consumers were asked to choose between WeChat and Apple Pay, 88% chose WeChat - and only 4% chose Apple. Apple's ecosystem of applications, which is very attractive to consumers in other countries, attracts little Chinese consumers, who receive everything they need from WeChat.

In India, Apple is also complicated.

According to Kantar , the 1.3 billion market, where functional phones still dominate, and Apple’s 7% annual GDP growth, accounts for 3% of the smartphone market. Of these 1.3 billion people, 70% live outside major cities, and 93% of rural residents have never made digital transfers in their lives.

Well, what's the problem, you ask - especially considering the fact that two thirds of the population is under 35?

The average price of a smartphone is $ 155 . Apple's plans for the production of smartphones in India suggest that they will sell for $ 455. Cheaper and better-quality smartphones made by Chinese OEMs currently occupy 51.4% of the market in India, an increase of 142% compared to last year. Mobile wallets schemes, caused by demonetization and independent of hardware, are quite popular. Paytm, supported by SoftBank and Alipay, has 200 million users and continues to grow. Oxigen, MobiKwik, PayU / Citrus Pay, as well as PayPal / network affiliate programs and card networks of Bharat QR codes, have the same initial position in the market, where phone hardware is largely the basis for digital payments that improve and simplify the financial part of the life of the Indian consumer.

After nine quarters of tracking 8,000 consumers per quarter, you can make a verdict.

Consumers in the US do not want a new payment method for the old method of calculation at the box office.

Instead, they, including the owners of the iPhone, want to develop a new scheme, in which there will not be the inefficiency of the method of paying for purchases in stores. They view connected devices as a way to use new payment methods.

In other words, consumers need a new payment method with a new method of calculation at the checkout.

The merging of online and offline worlds — and the possibilities for consumers to shop and pay for purchases, which I have written and told about since 2010, are not just empty words. This is a description of what consumers expect from digital payments.

And also what consumers use.

We can give just one example - a preliminary mobile order , which is extremely popular with all brands that have begun to use it. It accounts for more than 50% of transactions during peak loads, and the average order size increases by 20%.

It will also help determine the so-called winners and losers in mobile "wallets." Both in the US and around the world.

Or maybe already defined.

PayPal made friends with card networks and their issuers.

India has demonetized its currency and launched a program to introduce digital payments.

Amazon launched voice commerce with Alexa and a portfolio of applications and devices that now put it at the consumer’s disposal.

Selfie Pay has become a reality .

Walmart bought Jet.com to strengthen its e-commerce business.

The quick payment of piecework gave a strong impetus to the development of the economy of piecework earnings.

Payments bring us closer to the day when we can refuse checks ( #killthecheck ).

Efforts to combat fraudsters from the payment ecosystem have reduced online fraud by about a third.

But something has not been done in the past three years: consumers have not been stimulated to use smartphones as a digital form factor of payment when making payments in physical stores.

In fact, the results of PYMNTS / InfoScout “Implementation and use of mobile payments” for the last nine quarters say about the same as before: consumers do not have sufficient reasons not to forget to use them, although they usually hold the phone in one hand in the store while the other take out their plastic card in order to pay at the checkout.

Using Mobile Wallets

Let's clarify what we mean by “use”: this is the percentage of people who have a payment method on their phone, who pay in a terminal that supports this method, and, finally, those who actually use it to make a purchase.

The reluctance to exchange a leather wallet for an electronic one does not disappear, despite the proliferation of NFC-enabled terminals for “[insert the right name] Pay”, which requires contactless communication to initiate a payment - a rather sobering reality for the “grandfather” of all Pay - Apple Pay - despite the enthusiastic mention of Apple Pay by Apple CEO Tim Cook in their latest earnings report last week.

According to him, Apple Pay can be "currently the number one contactless payment service on mobile devices, which accounts for 90% of all transactions worldwide." But this is very similar to saying that you are the best of all troechnics in a troechnik class: it still remains a troechnik class.

Using Apple Pay

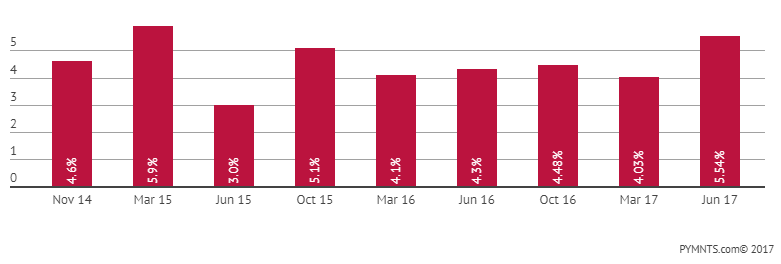

After nearly three years - after all the hype and huge investments in advertising and promotion - Apple Pay cannot count even 6% of its use in the largest payment market in the world.

According to our results, the average use over nine quarters is about 4.5%. Although a maximum of 5.9% was seen, and in the last quarter the figure reached 5.5%, the trend remains unchanged, despite growth in this quarter.

At this stage of his life cycle and the cycle of maturity, the question arises: Will he ever be able to break through this ceiling?

At the end of June, when the next survey was conducted, 24.5% of respondents said that they first tried Apple Pay, compared with 21.9% in March. And 5.5% said they used it to pay for purchases, which is higher than 4% in June, but lower than the maximum in March 2015

It is difficult to understand whether this is the beginning of a consistently growing trend or another jump, but statistically it looked like another random jump along a rather gloomy trend line. When we asked consumers how often they used Apple Pay to pay for a physical store, they responded that they did it about 18% of the time. Since March, this figure has not changed and continues to decline since October 2015.

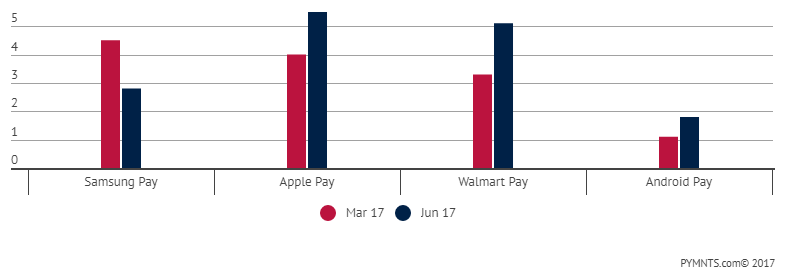

However, there is one exception to this story: Walmart Pay .

Since March, we have seen how the frequency of first use of Walmart Pay increased by 31.7% to 19.1% of respondents. The number of those who have an application on a smartphone and uses it for payment increased by 53.5% to 5.08% of respondents.

This jump is not interesting in itself, but because of the speed with which Walmart Pay forces those users who tried it for the first time to use it again. The use of 5.03% is observed after only 1 year on the market and this quarter only falls short of the Apple Pay figure of 5.5%, which is already on the market for the third year.

The frequency of using Walmart Pay is also an interesting story.

Nearly 50% (more precisely, 47.2%) of respondents who shop at Walmart say that they used it at every opportunity - only 6.6% said they never thought of using it.

However, this does not mean that before Walmart is not difficult tasks. Walmart Pay's biggest competitor is cash - it’s them, according to consumers, that they used instead of Walmart Pay, and many of them use it to make purchases so far. Ditto EBT cards that can not yet be registered in a digital wallet for payment. These are two big and important issues for Walmart Pay.

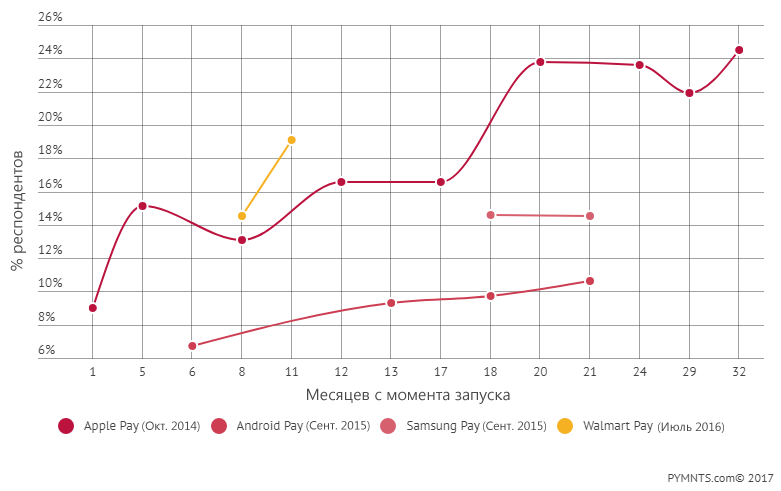

Use of mobile wallet: months from launch

However, it seems that the popularity of Walmart Pay does not lie in the very possibility to pay for purchases using the in-app application, but rather in the set of additional functions that accompany the payment process at the checkout.

But this is not even payment in the traditional sense of the word.

In fact, the QR code of Walmart Pay identifies the user before the start of the payment process, after which the consumer can put the phone back in the bag. The process of using coupons, promo codes, Savings Catcher bonuses and gift cards (if any) begins in the app, offering all the choices for the consumer until payment is complete. Walmart Pay also supports mobile grocery ordering, which will bring you to the car window, online purchases and in-store payment in cash, and now a number of financial services, including savings.

It all went much further than Apple Pay, which is still trying to complete this shopping quest (and, it seems, went the wrong way).

Integration of store loyalty programs in Apple Pay sounds tempting - until you get to the point where you still need to stand in line to get to the cashier and pay for it. At this stage, according to our respondents, the use of the card works great, especially since the use of card payment systems when paying for purchases at most stores today is quite fast.

You can say: wait, but after all, Tim Cook during the last teleconference on the company's financial activities, said that 3/4 of Apple Pay transactions occur outside the US, where, according to him, “the mobile payment infrastructure is developing faster than in the US ".

Despite the fact that all innovative payment innovations come from the US (if I read it out loud, you would hear a large share of sarcasm in my voice), can this country lag behind the ubiquitous contactless payment terminals for several years? According to statistics, 52% of US merchants accept contactless payments, including many successful small businesses, such as coffee shops and bakeries, that work with integrated terminals for sale, such as Clover and Square.

Unfortunately, this may not be the reason Apple Pay cannot win consumers in the US - although it could once be a good excuse for the low popularity of Apple Pay in its homeland - and, frankly, I was criticized when reviewing their early strategy. launch a payment system.

But what about those other global markets that account for 75% of Apple Pay transactions?

How much does Apple Pay account for, and where do consumers use it?

Maybe in the UK, where contactless payment is not very popular?

Maybe in Australia, where large banks tried to block Apple Pay, because they do not want to get into 15 bp. Apple Pay with their own contactless mobile wallets?

Maybe in Japan, where over the past 15 years, no mobile wallet has managed to gain popularity, and where the use of Apple Pay, as in the UK, seems to be a little popular?

Maybe in one of the new markets, such as Sweden or Denmark, where digital payments are an integral part of life, but where are local systems like Swish and Dankort, which are widely used and used today, so popular?

The short answer to this question is that we don’t know and may never know.

The likely answer to this question is unlikely, because if this were actually the case, Apple would have told about it.

Example: Even when Apple listed all the reasons for service revenue in its earnings report last week in response to an analyst's question, everything on this list except for Apple Pay. Nobody returned to this question anymore.

It is well known that Apple Pay is not used in China, where the company is betting on the future and where Apple Pay as a mobile payment solution puts users in touch with promotions and gifts to get them to try the system.

It is clear that China is a priority for Apple as the second largest economy in the world. There is only one problem: Apple has not become a top priority for China.

As a company, Apple has been losing sales in China since 2012, which fell by 10% in the last quarter, after a decrease of 14% from the previous quarter. Apple has a share of ~ 9% in the mobile phone market in China and a 0% share in the payments market (I think the numbers have just been rounded down!), According to a study conducted by China Channel . In China, Apple is considered a luxury brand, but now it’s one of the many phones that Chinese consumers buy to access the most important things for Chinese consumers: WeChat and the rest of the chat rooms, games, and commercial applications of the mobile ecosystem.

According to the China Channel report, 67% of Chinese consumers use QR codes from Alipay or WeChat Pay to pay at the store, 22% use UnionPay cards and 11% use cash (and zero percent use Apple Pay). When 4,000 Chinese consumers were asked to choose between WeChat and Apple Pay, 88% chose WeChat - and only 4% chose Apple. Apple's ecosystem of applications, which is very attractive to consumers in other countries, attracts little Chinese consumers, who receive everything they need from WeChat.

In India, Apple is also complicated.

According to Kantar , the 1.3 billion market, where functional phones still dominate, and Apple’s 7% annual GDP growth, accounts for 3% of the smartphone market. Of these 1.3 billion people, 70% live outside major cities, and 93% of rural residents have never made digital transfers in their lives.

Well, what's the problem, you ask - especially considering the fact that two thirds of the population is under 35?

Prices and Competition

The average price of a smartphone is $ 155 . Apple's plans for the production of smartphones in India suggest that they will sell for $ 455. Cheaper and better-quality smartphones made by Chinese OEMs currently occupy 51.4% of the market in India, an increase of 142% compared to last year. Mobile wallets schemes, caused by demonetization and independent of hardware, are quite popular. Paytm, supported by SoftBank and Alipay, has 200 million users and continues to grow. Oxigen, MobiKwik, PayU / Citrus Pay, as well as PayPal / network affiliate programs and card networks of Bharat QR codes, have the same initial position in the market, where phone hardware is largely the basis for digital payments that improve and simplify the financial part of the life of the Indian consumer.

So what does all this mean?

After nine quarters of tracking 8,000 consumers per quarter, you can make a verdict.

Consumers in the US do not want a new payment method for the old method of calculation at the box office.

Instead, they, including the owners of the iPhone, want to develop a new scheme, in which there will not be the inefficiency of the method of paying for purchases in stores. They view connected devices as a way to use new payment methods.

In other words, consumers need a new payment method with a new method of calculation at the checkout.

The merging of online and offline worlds — and the possibilities for consumers to shop and pay for purchases, which I have written and told about since 2010, are not just empty words. This is a description of what consumers expect from digital payments.

And also what consumers use.

We can give just one example - a preliminary mobile order , which is extremely popular with all brands that have begun to use it. It accounts for more than 50% of transactions during peak loads, and the average order size increases by 20%.

It will also help determine the so-called winners and losers in mobile "wallets." Both in the US and around the world.

Or maybe already defined.

All Articles